Butler National Corporation: Up Nearly 800% in a Decade, With More Room to Run

Far from being up in the air, a path to higher altitudes remains in the cards for BUKS stock.

Butler National (BUKS), a Kansas-based aerospace and casino gaming company, is a good example of how patience and a keen eye for value can produce strong returns for investors focusing on micro-cap stocks, particularly those listed in the over-the-counter (OTC) market.

Over the past decade, BUKS stock has gained by around 788%. The S&P 500 (excluding dividends reinvested) is up 172.7% over this same period. That said, it’s not as if these gains all arrived consistently. For many years, BUKS was dead money. I should know; back in late 2016, I entered a position, even wrote about it over on Seeking Alpha.

Although shares did benefit from a brief spike in 2017, it wasn’t until late 2019/early 2020, when favorable corporate developments, plus further price discovery from the market, pushed the stock to nearly 70 cents per share.

Around this time, I took profit. During the pandemic and post-pandemic era, shares experienced some volatility, but failed to make another breakout. This changed in 2024, when BUKS took off again, with the stock late last year hitting prices near $2 per share.

Since then, Butler National shares have pulled back slightly, to around $1.60 per share as of this writing. While I do not believe that another 10x move is in the cards, there may be merit in entering a position at or near current prices.

BUKS Stock: Background

Founded in 1960, Butler National is at its core an aerospace product and services company. Headquartered near the New Century Aircenter, a joint military-civil generation aviation airport located in New Century, KS, just outside Kansas City, the company’s main segment consists of several smaller companies in the aerospace industry or related industries:

Avcon: an aircraft modification product and services company.

Butler Avionics: aerospace equipment manufacturing, sales, installations, and service.

BNC-Tempe: a producer of industrial electronics for commercial and defense end-users.

KC Machine: a machine shop and machine tool repair company located in Excelsior Springs, Missouri.

Alongside the Aerospace/industrial segment, Butler National has a second segment, which it refers to as its “Professional Services” segment. That’s quite the euphemism, as this segment currently consists entirely of Butler National’s casino gaming operation, the Boot Hill Casino & Resort, located in Dodge City, KS. Alongside the casino itself,the company also has a sportsbook license. Butler contracts out sportsbook operations to DraftKings (DKNG), providing another lucrative profit stream for the Gaming unit.

Technically, Boot Hill, along with several other non-tribal commercial casinos in Kansas, are “owned” by the Kansas Lottery, with companies like Butler holding long-term contracts to manage the properties. However, over the past decade, Butler’s “management” of Boot Hill has become tantamount to full-on ownership.

Back in 2016, Butler National didn’t fully own BHCMC, the entity awarded the Boot Hill management contract. At the time, BUKS held an 80% equity interest and 60% profit participation interest in the entity, with a real estate developer holding not just the other 20% equity interest/40% profit participation interest, but owning the physical real estate of the casino as well.

Also, BHCMC’s contract to manage Boot Hill was set to expire in 2024. These factors weren’t the only reasons why investors were pricing BUKS at such as low valuation at that time. At that time, and up until very recently, Butler National’s CEO was like the poster child for entrenched management. Clark Stewart, who became BUKS’ CEO in 1989, managed to stay at helm for another 34 years, despite not holding voting control over the company.

This long tenure came despite a tremendous erosion of shareholder value during the 1990s and 2000s, worsened by Stewart’s high executive compensation relative to the company’s then-market cap, not to mention his employment of multiple family members in key and/or six-figure paying positions. Nice work, if you can get it.

The fact that Stewart and Co were still in charge in 2019/2020 was why I cashed out when the stock surged to 3-4x my cost basis. Even as news such as the Kansas Lottery’s extension of the casino management contract to 2039 helped to send BUKS higher, with incumbent management still running the show, it seems that further upside, likely realized from either a full sale of the company, or a sale of each of its two business units, was not on the horizon.

However, hindsight is 20/20, literally 2020 in this case. At the start of this decade, Butler made two major moves that solidified the company’s de facto ownership of Boot Hill. First, in late 2020, Butler bought Boot Hill’s physical real estate for $42 million. Second, Butler bought out the developer’s minority interest in Boot Hill, for $16.4 million.

Although Butler had to take on additional leverage to complete these transactions, this quickly proved to be a profitable move, and played a major role in BUKS’ big jump in profitability during the fiscal year ending April 2022.

That year, operating income surged from $2.5 million to $12.2 million, and earnings per share increased by seven-fold, to 14 cents per share.

The following fiscal year, earnings took a moderately-high hit, but this was largely due to a one-time expense related to a game-changing development for Butler National. For FY2023, the company reported a $4.5 million severance accrual, related to exit of Clark Stewart and Craig Stewart (Clark’s son), from the CEO and Aerospace Divsion President roles.

Besides receiving severance, Stewart and son sold their 7.9% interest (5.8 million shares) in BUKS back to the company, at an average price of 73.9 cents per share. Following the Stewart family’s exit, longtime Butler exec Chris Reedy took the helm.

Since this C-suite shakeup, shares have gone on another strong run, this time for reasons primarily related to per-share earnings growth.

Recent Developments

During FY2024, profitability bounced back, coming in at $12.5 million, or 18 cents per share. A few million of this came was the result of one-time asset sales, but excluding these items, after-tax earnings were around $8.05 million, or around 11.4 cents per share.

In more recent quarters, revenue and earnings have experienced an additional growth boost, mainly due to growth with Butler’s aerospace businesses. Last quarter, while gaming revenue came in flat on a year-over-year basis, aerospace sales grew nearly 26% compared to the prior year’s quarter. Contract backlog increased to $35.2 million, up from $30.4 million a year prior.

BUKS’ move to between $1.50 and $2 per share may reflect these improving results, but don’t assume the opportunity here has fully come and gone. A closer look at Butler’s valuation suggests further significant value could be unlocked by the company.

Butler National Valuation

At current prices, Butler National Corporation has a $108.06 million market cap, total debt of $40.49 million, and total cash of $30.7 million, giving BUKS a total enterprise value of $117.84 million. Based on TTM EBITDA of around $23.6 million, this means that Butler National, even after an incredible run-up in price, remains undervalued, at an EBITDA multiple of just under 5.

Just back-of-the-envelope, we can see how cheap BUKS is to public peers. Most aerospace companies are trading at EBITDA multiples in the low-teens right now. As for the casino business, with Butler owning and operating the facilities, we can value these using what’s known as the “opco/propco” multiple, or EBITDA multiple that accounts for both ownership of the casino operating business, plus ownership of the physical real estate property.

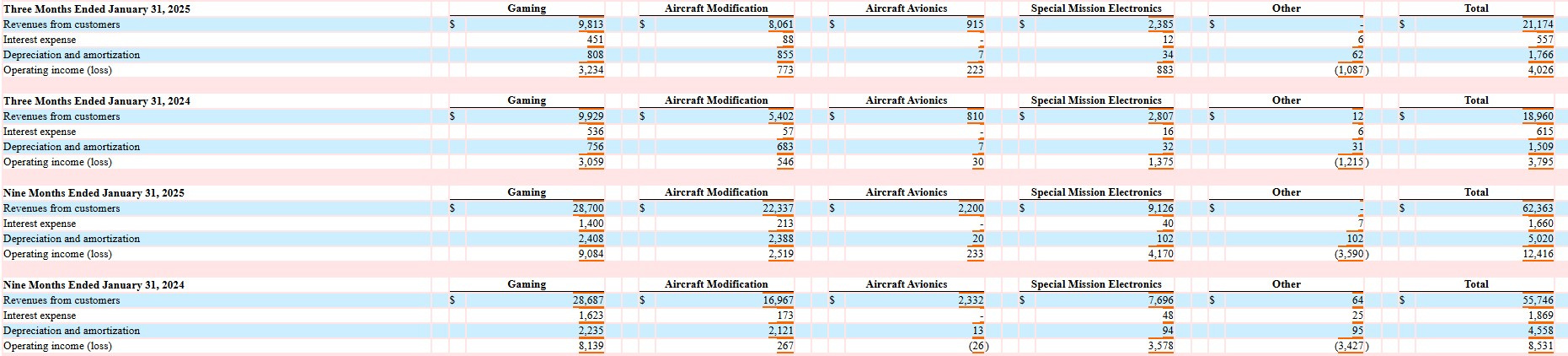

As seen in the table above from BUKS’ latest 10-Q filing, we can determine segment EBITDA, and from there determine an approximate valuation for Butler National’s two operating segments.

Over the past nine month period, Butler National’s corporate expenses have totaled $3.59 million. This suggests annual corporate overhead of around $4.8 million. We’ll apply portions of this corporate overhead to each operating unit, proportional to each unit’s EBITDA.

Based on the figures listed under “operating income” and “depreciation and amortization,” we can see that the Gaming unit had EBITDA of around $4 million last quarter, and around $11.5 million over the past nine month period. This suggests annual EBITDA of at least $15 million.

As for Aerospace, over the past nine months, Butler’s collection of aerospace product and service companies generated a total of $9.43 million in EBITDA, or around $12.6 million annualized.

With around 54% of EBITDA attributable to Gaming, and 46% to Aerospace, we’ll deduct $2.6 million from Gaming and $2.2 million from Aerospace, to account for overhead.

Adjusting for overhead, this gives us around $12.4 million in annual EBITDA for gaming, and $10.4 million for Aerospace.

Looking at comparable regional casino “opco”/"propco” deals, or deals where a regional casino company buys the operations of a property, while an entity like a casino REIT buys the property, we can see that Butler could in theory fetch a high price for Boot Hill.

For example, in 2022, when Golden Entertainment (GDEN) sold its Rocky Gap Casino Resort property in Maryland, Century Casinos (CNTY) paid $56.1 million for the operations, while VICI Properties (VICI) paid $203.9 million for the real estate.

This $260 million deal valued the property at a blended valuation of 10x EBITDA. In turn, Boot Hill could be worth around $125 million, if such a deal was completed.

With $10.4 million in annual EBITDA, I believe this business could sustain a high single-digit EBITDA multiple, near the valuation of similarly-sized publicly-traded aerospace names. Here a few examples:

Optex Systems Holdings (OPXS), currently trading at a 6.6x EBITDA multiple.

Environmental Tectonics (ETCC), currently trading at a 8.3x EBITDA multiple.

CPI Aerostructures (CVU): currently trading at a 9.79x EBITDA multiple.

Innovative Solutions and Support (ISSC): currently trading at a 11.1x EBITDA multiple.

Averaging these, we get a 9x EBITDA multiple, or around a $93.6 million valuation.

Adding it all together, $125 million for the Gaming business and $93.6 million for the aerospace unit gives us $218.6 million gross value for both of Butler’s busineses. Subtract the $40.5 million in debt, add back $30.7 million in cash, and we get a net value of around $208.8 million, or just under $3.10 per share, more than double the current stock price.

Unlocking Butler’s Additional Value

With little question about additional value with BUKS stock, the challenge is whether another material move will happen within a reasonable time frame. My prior talk of patience notwithstanding, it’s not as if we want to buy BUKS, only for it to reach $3 per share a decade from now.

In this scenario, “reasonable time frame” still entails a multi-year time frame. Barring another growth surge for the aerospace unit, it may take financial engineering to drive the next big rally. Fortunately, the ingredients may be in place for Butler to pull this off.

First, assuming Butler continues using its cash flow to repurchase shares, the resultant per-share earnings growth alone may be enough to drive an additional move higher. Second, and admittedly a bit more speculative, Butler could be positioning itself to become an aerospace pure play.

With the gaming business now lagging aerospace in terms of growth, it may be high time for BUKS to divest this asset. A spin-off may be the best move, from a tax efficiency perspective. For instance, perhaps Butler could split off Boot Hill, through a reverse Morris Trust spinoff, where Boot Hill is merged into another micro-cap casino company, with Butler distributing the majority stake to its shareholders.

By turning Butler into an aerospace pure play once again, the market could reward this faster growing standalone business with a higher forward valuation. The company could also consider becoming a rollup vehicle in aerospace, acquiring small and similarly-sized competitors in the space.

Acquiring additional scale, Butler could then consider making a move up from the OTC markets, to a major exchange like the NASDAQ. With a major market listing, and greater public awareness, shares could reach even loftier price levels, thanks to continued multiple expansion.

Who knows, investor sentiment could in this scenario eventually take the view that Butler is the next Transdigm (TDG), a more well-known aerospace serial acquirer, whose shares have experienced tremendous price appreciation since the 2010s.

Risk, Uncertainty, and the Bottom Line

Although there is a path for this OTC-listed winner to level up on its gains, don’t discount the risk of another sharp drawdown. Any sort of quarterly earnings stumble or reported decline in contract backlog could cause shares to cough back a healthy portion of their recent gains.

It’s also far from a given that Butler either sells or spins off its casino business. There has not been any public statement from the C-suite regarding this. Without a casino sale, investors could continue to apply a “conglomerate discount” on BUKS.

Still, while you may be hesitant to buy BUKS stock after its latest super-rally, given its low valuation downside risk may be far less substantial than you think. Even if asset sales/a spinoff fail to happen, Butler’s continued repurchasing of shares could add additional upward pressure for the stock.

You may want to wait for a pullback before backing up the truck, but consider Butler National worthy of a buy at current prices.

DISCLOSURE: As of Publication, The author (Thomas Niel) held a position in BUKS.

DISCLAIMER: I wrote this article myself, and it expresses my own opinions. I am not receiving compensation from BUKS or any other entity for writing this article. I have no business relationship with BUKS, or any other company referenced.This article is for informational purposes only, and should not be construed as investment advice. Please consult your financial advisor before making any investment decision. Please be aware of the risks associated with trading BUKS stock. Do your own due diligence, and caveat emptor.