SunLink Health Systems (SSY): Many Paths to Upside With This Nanocap Merger Arb Situation

Between a hefty deal spread, potential for post-merger gains, and the opportunity to pursue other avenues to maximize value if the deal falls through, consider taking a look at SSY stock.

SunLink Health Systems (NYSE:SSY) was at one point involved in multiple aspects of the health care sector. More recently, however, the company, which many in the micro-cap/nanocap space are likely aware of, has sold off the majority of these business units.

Following these asset sales, SSY now owns just one operating business: Carmichael’s Cashway Pharmacy, a 4-unit chain in southwestern Louisiana. Moreover, the former acquirer has been an acquisition target. On Jan. 6, 2025, Regional Health Properties (OTCMKTS:RHEP), a healthcare REIT, announced plans to acquire Sunlink, in an all-stock transaction.

Although SSY stock surged on the news, an outsized deal spread remains, albeit a complex one that may make the situation more risky than other merger arbitrage plays. Moreover, completion of this announced deal may not be the sole path to upside.

Why? Regional Health could successfully use SSY’s cash position, as well as the sale of its remaining assets, to finance its turnaround. Although risky, the end result could be tremendous price appreciation, for both RHEP and SSY investors.

Even in the off chance the deal fails to go through, an position in SSY may not be doomed, as the company, trading at a sharp discount to its liquidation value, could pursue other ways to realize its underlying value.

SSY Stock: Hefty Deal Spread, but With Some Caveats

Per the terms of the merger agreement, investors in SSY stock are getting 1 newly-issued share of RHEP common stock, as well as 1 share of RHEP’s series D 8% cumulative convertible preferred stock, for every five shares of SSY.

While the convertible shares convert to common on a 1:3 basis, or one share of RHEP common for every 3 shares of RHEP series D convertible preferred, they do have a liquidation preference of $10 per share. 1.41 million series D shares are set to be issued, equating to a total liquidation preference of $14.1 million.

It should be noted that another series of outstanding preferred, series B, trades at a discount to its liquidation preference. At current prices, OTCQB-listed RHEPB stock trades for around $6.25 per share.

Still, even if we assume that the series D shares would trade at a similar discount in the public market, buying SSY now, and holding on until the deal closes within the next few months, could still generate worthwhile gains.

At current prices, SSY trades for $1 per share. Based on merger terms, if SSY investors are getting 0.2 shares of RHEP common, trading for $1.26 per share today, and 0.2 shares of RHEPD, which could trade for $6.25 per share once its trading in the public markets, this implies SSY investors will receive securities worth ~$1.50 per share.

That's a hefty deal spread, for a transaction that could be weeks away from completion. The effective deal spread could end up being even higher. As Sunlink noted in the merger press release, the company intends to issue a final special dividend to shareholders prior to the merger.

Yes, this particular situation highlights why they often call merger arbitrage “risk arbitrage." Because of RHEP’s low stock, shorting its common shares, for hedging purposes, may prove difficult. Hence, there’s a possible risk of capital loss, if RHEP shares keep sinking between now and the merger completion date.

RHEPD could end up having a far greater valuation discount priced-into it than RHEPB, if only due to the series B sporting a 12.5% cumulative dividend, versus an 8% cumulative dividend for RHEPD.

A Challenging Path Ahead for Post-Merger Gains

As stated in the deal announcement press release, SunLink and Regional anticipate that the merger will create $1 million in annual pre-tax cost savings by 2026. Given the small size of both companies, this may at first sound like a possible needle-mover.

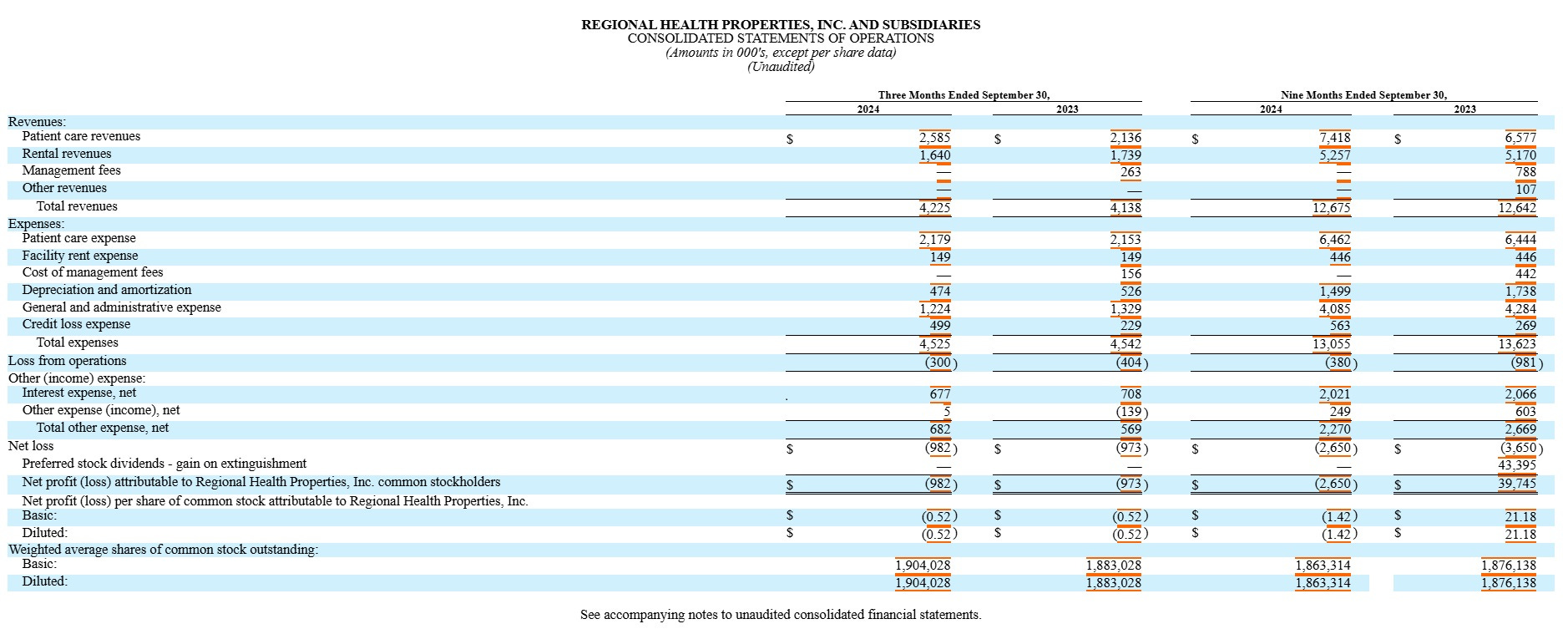

However, while Regional Health Properties is profitable on an EBITDA basis, with a TTM EBITDA of $1.8 million, that’s not the story with SunLink. Last quarter, SSY reported negative EBITDA of $700,000, and operating losses of around $1 million.

Over the TTM period, EBITDA for Sunlink’s operating business was around $2.4 million, while operating losses came in at around $3.8 million. With this in mind, plus taking into Regional’s own headwinds, a multistep plan will likely need to be pursued, in order for this merger to unlock significant value.

First, once the deal is completed, Regional should figure out how to divest Carmichael’s Cashway. Although unprofitable, a large strategic buyer may be willing to pay at least book value for this business. Effectively completing the full liquidation of SunLink, a sale of Carmichael’s would likely provide Regional more capital. This capital could be put to work paring down debt or buying back outstanding preferred stock.

Second, a few years from now, the company may get a shot at taking another big slice out of G&A costs. Regional CEO and President Brent Morrison is tapped to stay on in the same roles, but Robert M. Thornton Jr., SunLink’s CEO, will continue to be a member of the C-suite, with the job title of Executive VP-Corporate Strategy. Mark Stockslager, Sunlink’s CFO, is coming on to be the CFO of the combined company.

Third, there is something else that could play out, at the same time that the first two. RHEP both owns skilled nursing facilities that it leases out to third parties, as well as directly operates two facilities.

Based on Regional Health Properties’ latest quarterly results, it’s clear that its the directly-operated segment is what’s been driving the losses. If the company could divest of these operations as well, I can see a scenario where RHEP strips down to its core triple-net lease senior living and SNF properties, using the assets received from the SunLink deal, as well as cash flow, to pay down debt and redeem preferred stock.

Separate out the rental business, and its clear that RHEP is generating positive operating income from its property portfolio. Rented out on a NNN basis, these properties produce around $1.49 million in NOI per quarter, just under $6 million annually.

Using EBITDA multiple as a proxy for cap rates, and taking a look at the valuation of smaller healthcare REITs, I believe an EBITDA multiple of 13x-15x, or somewhere around an effective cap rate in the 7% range, is a fair valuation for these assets. This translates into a valuation of around $85 million gross value for the business.

Regional Health Properties has around $49.7 million in outstanding debt. If Regional were to sell SSY’s last remaining operating business, enabling it to fully tap into the acquisition target’s $12.9 million in net tangible assets, these proceeds could be used to reduce RHEP’s debt position down to around $36.8 million.

Subtract $36.8 million from $85 million, and we get a net value of around $48.2 million for RHEC. Factor in the liquidation preferences of the series B ($18.6 million), the upcoming series D ($14.1 million), as well as the small amount of series A prefs still outstanding (liquidation preference of $426,000, and we an estimated value for the common shares of around $15 million.

Following the merger, RHEP’s common share count will rise from 1.79 million to 3.2 million. At a $15 million valuation, RHEP would be trading for around $4.43 per share. That’s more than three and half times RHEP’s current stock price.

If SSY investors receive 0.2 shares of RHEP, and 0.2 shares of RHEPD, it’s not inconceivable that their equity position could be worth the equivalent of around $2.89 per share several years down the road, nearly three times that of current prices.

Of course, this is more of a “best care scenario” than the most likely way RHEP’s future plays out. Even if RHEP is successful unloading unprofitable operations, keeping its profitable REIT core, the company may have to raise millions in capital to absorb losses/finance this transformation. The resultant dilution could limit long-term upside for those deciding to let it ride post-merger.

Regional Health is also paying dividends on its series B preferred using common stock, and will likely do the same with the series D preferred. This will result in additional shareholder dilution. In short, while

Alternate Path to Gains if Deal Falls Through

Owning SSY stands to be profitable in the near-term as a merger arb, and possibly be even more profitable following the merger close, but what happens if the deal falls through?

SSY stock could undoubtedly experience a sharp correction on the onset, if such a scenario began playing out. Still, even if SSY were to stumble back towards its 52-week low, the company could decide to pursue other “strategic alternatives,” like a liquidation.

If successful in selling off the pharmacy business, SSY would have not just its $8 million cash position, but the proceeds from one last asset sale. In the above example about a post-merger SunLink/Regional, I talked about the combined entity being able to divest Carmichael’s for an amount that would enable SunLink to fully realize its current tangible asset value. In other words, around $4.9 million.

SunLink paid $24 million for Carmichael’s back in 2008. Given the poor fiscal performance, I don’t believe it’s worth anything near this prior figure. Again, however, I believe that a strategic acquirer may consider book value a worthwhile purchase price, perhaps even a bargain price.

With the segment generating annual revenue in the low-$30 million range, at $4.9 million a financial or strategic acquirer would be getting this business for 0.16x sales. For comparison, Walgreens Boots Alliance (WBA) currently trades at an EV/Sales ratio of 0.27x.

Even if Carmichael’s were to be sold at an even lower valuation, the end result would likely still lead to turning SSY into a “cash box” worth more liquidated than in business. To realize potential gains, management could issue one or several special liquidating dividends. While operating losses and other expenses would likely eat up a portion of the tangible book value, a liquidation of SSY could produce solid returns relative to the time frame.

Bottom Line on SSY Stock

With not one, not two, but three potential paths to major upside, investors in OTC-listed stocks may want to consider accumulating up an SSY stock position at current prices. If market volatility strikes again in the near-term, the opportunity to buy a position at an even more favorable entry point could emerge.